How Much Does It Cost to Open a Mechanic Shop?

Opening a modest mechanic shop usually takes $75,000 to $150,000 in startup capital. A standard two-bay setup often lands in that range, and once the shop gets larger, the required cash climbs fast.

That headline number answers the search query, but it doesn't answer the harder question owners run into after signing a lease and buying equipment. The primary challenge isn't just getting a lift installed or buying a scanner. It's making sure the business has enough cash to survive the slow first stretch, when payroll, rent, utilities, parts, and admin work keep moving whether cars are in the bays or not.

A lot of new owners budget for tools and build-out, then get squeezed by the gap between opening day and steady car count. That's where shops get into trouble. Good technicians still lose money when the front office is disorganized, approvals stall, parts aren't tracked well, and cash leaves faster than it comes in. The cost to open a mechanic shop is never just a setup number. It's startup capital plus operating discipline.

Table of Contents

- The Real Answer to Your Million Dollar Question

- Sample Startup Budgets Low Medium and High

- Your One-Time Startup Expense Checklist

- Calculating Your Monthly Operating Costs

- Surviving the Pre-Breakeven Cash Flow Cliff

- Smart Spending and Securing Your Funds

- Your Action Plan for Budgeting and Launch

The Real Answer to Your Million Dollar Question

Those asking how much does it cost to open a mechanic shop want one clean number. The honest answer is a range, and that range depends on bay count, service mix, location, and how much cash the owner keeps in reserve instead of spending every dollar before opening.

For a modest shop, the practical starting point is the lower six figures or just under it. A barebones operation can open lean, but that usually means tighter limits on equipment, less room for staffing mistakes, and almost no cushion if revenue starts slowly. Once a shop adds more bays, broader service capability, and more inventory, the budget moves up quickly.

The part many owners underestimate isn't skill. It's liquidity. A shop can be full of talent and still run into trouble if the owner spends heavily on tools, signs the lease, and doesn't leave enough working cash in the bank.

Practical rule: The opening budget gets the doors unlocked. Working capital keeps them open.

That distinction matters because startup advice often focuses on the visible items. Lifts, scanners, compressors, branding, desks, and waiting-room furniture are easy to price. The harder part is planning for the first stretch of uneven workflow, delayed approvals, warranty work, slow-paying fleet accounts, and the normal lag between estimate and collection.

A simple way to look at it is:

- Startup capital covers the shop setup, equipment, deposits, initial inventory, and launch work.

- Operating cash covers the months when expenses are real but sales are still building.

- Financial control determines whether the owner converts work into cash fast enough.

A shop owner doesn't need the fanciest operation on day one. The owner does need a budget that reflects reality. That means choosing a size that can be financed without starving the business for cash, keeping the service offering focused, and setting up the front office well enough that estimates move, parts are billed correctly, and labor isn't lost in the shuffle.

Sample Startup Budgets Low Medium and High

Shops rarely fail because the owner mispriced a lift. They fail because the opening budget covered setup, but not the working capital gap between opening day and steady cash collection.

Bay count still matters, but cash timing matters more. A one or two-bay shop can survive on a tighter setup if the owner keeps overhead low and invoices turn into cash fast. A larger facility gives you more production capacity, but it also raises the amount of money tied up in rent, payroll, parts, insurance, and slower receivables before the shop settles into a rhythm.

Low budget lean owner operator model

A low-budget startup usually means a small leased space, one or two lifts, the owner on the floor every day, and limited front office payroll. The U.S. Small Business Administration notes that startup costs for an auto repair and body shop can range from about $50,000 to $100,000, depending on size, equipment, and location, in its.

That lower range works best when the service mix is narrow and the owner already knows how to control labor time, parts ordering, and collections. The trade-off is pressure. One slow month, one engine job that stalls, or one insurance payment delay can tighten cash quickly.

I usually tell first-time owners to treat the low-budget model as a discipline test. If the shop cannot stay organized with a simple setup, adding bays will not fix it.

Medium budget standard two-bay shop

The middle range is where many independent shops should start their planning. Analysts at Fit Small Business estimate that opening an auto repair shop often runs from $95,000 to $250,000, once you account for leasehold improvements, equipment, tools, licenses, and opening cash reserves, in their auto repair shop startup cost guide.

A realistic two-bay operation often lands somewhere in that broader range. It can support a professional front counter, enough equipment to avoid obvious bottlenecks, and a cleaner customer experience. It also creates a better margin for error if one tech is slow to ramp up or if car count builds unevenly in the first few months.

This is also the point where software starts paying for itself. Shop management systems help owners close estimates faster, track labor accurately, bill parts correctly, and collect sooner. Those are cash flow controls, not administrative extras.

High budget multi-bay advanced facility

A high-budget shop usually means several bays, more equipment, a wider service menu, stronger curb appeal, and higher fixed overhead from day one. GenSteel's review of repair shop build and setup costs shows how quickly facility size, steel building costs, lifts, diagnostic gear, and outfitting can push total investment upward for larger operations in its.

This model can make sense for an operator with an existing customer base, fleet relationships, or a proven specialty such as diagnostics, diesel, transmission, or high-volume general repair. It gets risky when the owner assumes extra bays automatically produce revenue. They do not. Empty bays still generate rent, utilities, insurance, and equipment payments.

Insurance planning also gets more expensive as the operation grows, especially if you store customer vehicles overnight. Owners in that market should review these while building the budget.

| Budget tier | What it usually supports | Main trade-off |

|---|---|---|

| Low | Small footprint, owner-led labor, basic equipment | Very little room for cash flow mistakes |

| Medium | Two-bay setup, stronger process, more balanced opening budget | Higher startup requirement, but better operating stability |

| High | Multi-bay facility, broader capability, stronger capacity | Fixed overhead rises fast if volume lags |

The right starting budget is the one that leaves enough cash in reserve to bridge the first stretch of uneven sales, delayed approvals, and slow collections. That is the number many new shop owners miss.

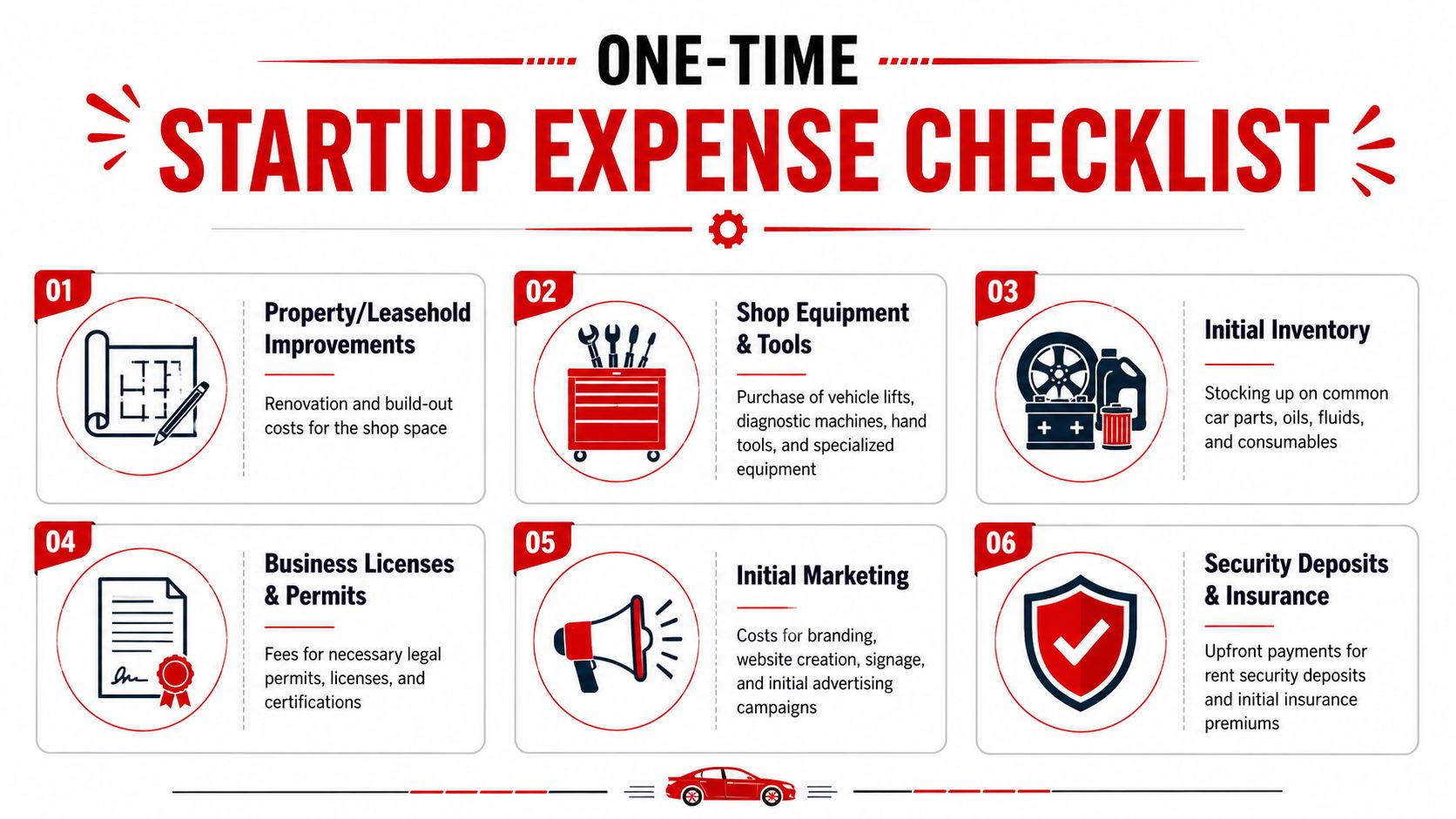

Your One-Time Startup Expense Checklist

A startup budget fails faster from missed opening costs than from obvious big-ticket items. I see it all the time. The owner prices lifts and tools correctly, then gets squeezed by deposits, software setup, signage, permit fees, and the first insurance bill before the first profitable month arrives.

Equipment that can't be skipped

The core equipment costs are usually the clearest part of the budget. Essential mechanic toolsets require about $15,000, a single hydraulic lift costs around $3,700, and diagnostic machines range from $5,000 to $10,000, based on.

Those numbers shape your opening model. A shop that cuts too hard on scanners, lifts, or air systems usually loses the savings later through slower turnaround, weaker diagnostic accuracy, and more rework. I would rather see a new owner start with a plain front office and buy the right diagnostic coverage than overspend on appearance and underbuy the tools that produce hours.

A practical one-time equipment list usually includes:

- Professional toolset: The base requirement for productive labor.

- Vehicle lifts: Bay count and service mix drive this cost.

- Diagnostic equipment: Scanner capability should match the vehicles you plan to service.

- Compressor and support equipment: Air tools, tire work, and daily shop function depend on it.

- Initial parts and fluids stock: Fast-moving items keep cars from sitting in bays waiting on basics.

Facility costs owners often miss

The building creates some of the largest opening checks, and many first-time owners underestimate how much cash gets tied up before revenue starts. Security deposits, advance rent, utility deposits, basic paint and repairs, front-counter setup, and exterior signage all hit before the schedule is full.

The U.S. Small Business Administration notes that startup costs often include deposits, licenses, inventory, equipment, and rent before opening in its. That matters because these expenses do not just raise the total budget. They also drain the working capital bridge you need for the first few uneven months.

Owners should also budget for setup items that look minor on a spreadsheet but show up fast in the bank account.

| One-time item | Why it matters |

|---|---|

| Build-out work | Makes the space usable for repair flow, customer intake, and code compliance |

| Waiting area setup | Gives customers a clean, professional first impression without overspending |

| Security systems | Reduces risk around stored vehicles, keys, and tool theft |

| Office hardware | Supports estimates, invoicing, parts ordering, and daily communication |

| Signage and launch branding | Helps local drivers find the shop and trust it enough to book |

A clean, organized facility does more than look professional. It shortens setup delays and helps the shop start billing work faster.

Insurance permits and setup details

Insurance belongs on the one-time checklist because many carriers collect a sizable payment upfront, not after the cash starts coming in. The same goes for licenses, local permits, waste-handling registration, and initial merchant account or payment processing setup.

Coverage choice matters as much as premium size. If you plan to keep customer vehicles overnight, you need to understand custody risk before opening the doors. These explain the exposure clearly.

Software setup should be in this checklist too. Shop management software, digital inspections, estimating tools, and parts integration are opening costs, but they also protect cash flow. A good system helps the front counter approve work faster, collect deposits, track parts status, and close tickets without billing delays. That does not remove the need for a cash reserve. It does reduce the small process failures that leave new shops short on cash at the worst time.

The owners who open cleanly are usually the ones who treat startup spending and working capital as one plan, not two separate budgets.

Calculating Your Monthly Operating Costs

A new shop can look busy and still run short on cash. Monthly operating costs are where that happens.

For a small to mid-sized mechanic shop, the recurring expense load usually lands in the low five figures each month, and it climbs fast once payroll, rent, insurance, software, and parts ordering all hit at the same time. For many 3-to-5 bay shops, the question is not whether overhead exists. The question is how many weeks of weak car count or slow collections the shop can absorb before cash gets tight.

What keeps running every month

Owners usually know the major categories. What they often underestimate is the timing. Payroll comes due on schedule. Rent comes due on schedule. Vendor bills show up before every repair order has been closed and collected.

The monthly cost stack usually includes:

- Rent or mortgage payment: Fixed and unforgiving, especially in high-traffic retail or industrial space

- Payroll: Technicians, advisors, payroll taxes, and any support staff

- Utilities and shop services: Power, compressed air, water, internet, waste oil pickup, laundry, and disposal fees

- Insurance: Garage liability, workers' comp, property coverage, and any required endorsements

- Software subscriptions: Shop management, inspections, estimating, accounting, and payment processing tools

- Marketing: Local search, reviews, paid ads, mailers, or community promotions

- Parts and materials: Daily parts purchases, shop supplies, fluids, sublet work, and returns that tie up cash

Payroll and occupancy usually do the most damage when revenue slips. Parts are the category that catches new owners off guard. A shop can post solid sales on paper and still feel squeezed if too much cash is sitting in parts, cores, unbilled labor, or jobs waiting on approval.

That is why working capital matters as much as the expense total itself.

Where overhead gets controlled

Healthy shops track overhead at the process level, not just on a profit and loss statement at month-end. I tell new owners to watch the points where cash slows down: delayed write-ups, inspections that never turn into approved work, parts ordered before commitment, supplements that never get billed, and invoices that stay open too long.

To keep monthly costs from turning into a cash trap, the operation needs discipline around:

- Vehicle intake so the advisor captures the full concern and sets up a billable inspection path

- Digital inspections so the customer sees the work clearly and approves faster

- Estimate follow-up so recommended jobs do not sit in limbo for days

- Parts control so special orders, returns, and cores are tracked tightly

- Invoice accuracy so labor, fluids, diagnostics, fees, and materials all make it onto the ticket

- Collections so completed work turns into deposited cash without delay

A lot of first-time owners focus on total sales and miss cash velocity. That mistake is expensive.

A modern shop management system helps close that gap. It gives the front counter a cleaner handoff from inspection to estimate, shows job status in real time, flags missed line items, and shortens the gap between finished work and payment. Software does not lower rent or payroll. It does reduce the routine leaks that make monthly overhead harder to carry.

Shops that stay stable early on usually share the same habit. They treat monthly operating costs as a cash flow management problem, not just a budgeting exercise.

Surviving the Pre-Breakeven Cash Flow Cliff

A new shop can open with a full schedule on paper and still run out of cash before the sales pace catches up to payroll, rent, and parts bills. That gap is what kills more first-time shops than a bad location or weak wrenching.

The danger period is the first stretch after the doors open. Money is going out on a fixed schedule. Money coming in is uneven. Customers delay approvals, commercial accounts pay on terms, comeback work eats technician time, and special-order parts can tie up cash before the invoice is closed. I have seen owners spend heavily to get the shop launch-ready, then realize they funded the opening and forgot to fund the first few months of operation.

recommends holding 3 to 6 months of liquid capital to cover the period before the shop reaches stable breakeven. That reserve belongs in a separate working capital bucket. If it gets mixed into the build-out and equipment number, it usually disappears into lifts, signage, and opening inventory.

Why the cash gap gets underestimated

New owners usually build the startup budget around visible expenses. Lease deposit. Paint. Alignment rack. Tire machine. Front counter. Those costs are real, but they are one-time decisions.

The harder problem is the working capital bridge.

A shop can post decent sales and still be tight on cash because the timing is wrong. Payroll hits this Friday. The landlord drafts rent on the first. The parts statement is due at month-end. Meanwhile, some repair orders are still waiting on approval, some invoices are sitting unpaid, and some larger jobs have not turned into collected cash yet. Busy is not the same as funded.

Software helps here more than many owners expect. A modern shop management system shortens approval time with digital inspections, reduces missed billed items, tracks parts status, and gets invoices closed faster. It does not remove overhead, but it does reduce the delay between labor performed and cash collected. Early on, that timing matters as much as sales volume.

Build the reserve as its own line item

Set up the startup plan in two buckets and protect the second one.

| Bucket | Purpose |

|---|---|

| Opening budget | Lease, build-out, tools, lifts, equipment, insurance, licenses, initial setup |

| Working capital reserve | Payroll, rent, utilities, parts vendors, software, and normal operating losses before breakeven |

That reserve is not spare money. It is the runway that keeps a slow first quarter from turning into a shutdown.

Owners who finance the launch should also understand what their debt service will do to monthly cash needs. If you are comparing funding options, this is a practical place to review how loan structure affects payments, use of funds, and qualification.

What a real cash buffer protects you from

The first reserve buys time for a few common problems:

- Slower-than-expected car count in the first 60 to 90 days

- Lower approval rates while the shop is still building trust and reviews

- Commercial accounts that pay on terms instead of at pickup

- Parts returns, warranty rework, and other cash-draining friction

- Hiring ahead of sales so the shop can handle booked work

A disciplined owner treats that reserve as off-limits unless it supports operations. Another scanner can wait. Better waiting-room furniture can wait. The cash bridge usually cannot.

Smart Spending and Securing Your Funds

The first bad spending decision usually is not buying too much equipment. It is using cash that should have stayed in the working capital bridge.

I see that mistake often with first-time shop owners. They spend heavily to open with a polished front office, extra specialty tools, or more bays than current demand can support. Then the shop gets busy enough to create payroll, parts, and vendor pressure, but not busy enough to collect cash fast. That gap is what puts a new garage in trouble.

Spend based on payback, not pride

Buy the items that help the shop inspect cars accurately, build estimates quickly, finish work on time, and collect payment without delay. Delay the purchases that mainly improve appearance or satisfy a future vision of the business.

Used equipment often makes sense if it is dependable and easy to service. Front-office furniture, shelving, and other non-revenue items are good places to save. Lifts, alignment equipment, scan tools, air systems, and anything that can stop production deserve a stricter standard. One breakdown on a core piece of equipment can cost more in lost labor sales than the purchase discount ever saved.

Software belongs in the same conversation. Shops that set up inspections, estimates, approvals, invoicing, and follow-up properly usually protect cash better than shops that focus only on shaving startup costs. RedAppy's analytics can help owners see technician efficiency, approval trends, and revenue leaks early. That matters because cash flow problems usually start with weak process control, not one oversized supply order.

Fund the shop in layers

Most owners use a mix of cash, term debt, and equipment financing. That is usually healthier than forcing one source to carry everything.

A practical approach looks like this:

- Use cash for deposits, licensing, insurance setup, and early operating needs

- Use equipment financing for assets that will earn for years

- Use term financing carefully when it preserves the reserve

- Keep enough liquidity to cover delays in ramp-up, not just opening day

The loan structure matters as much as the loan amount. A lower payment can protect the cash bridge in the first year, while a short amortization can squeeze it. If you are comparing options, this is a practical resource for understanding use of funds, qualification, and how repayment terms affect monthly pressure.

Protect cash by tightening the operating system

Shops rarely spend their way into trouble in one big moment. They bleed into it through slow estimates, missed approvals, weak parts controls, poor follow-up, and late collections.

That is why smart spending and cash management belong together. The owner who buys a slightly smaller setup but installs disciplined shop management software often has the stronger business. Faster estimate approvals, cleaner invoices, better scheduling, and tighter reporting shorten the time between labor performed and cash collected.

The goal is simple. Put money into the tools, equipment, and systems that help the shop bill accurately, move cars through the bays, and get paid on time. Protect the working capital bridge while the business earns its footing.

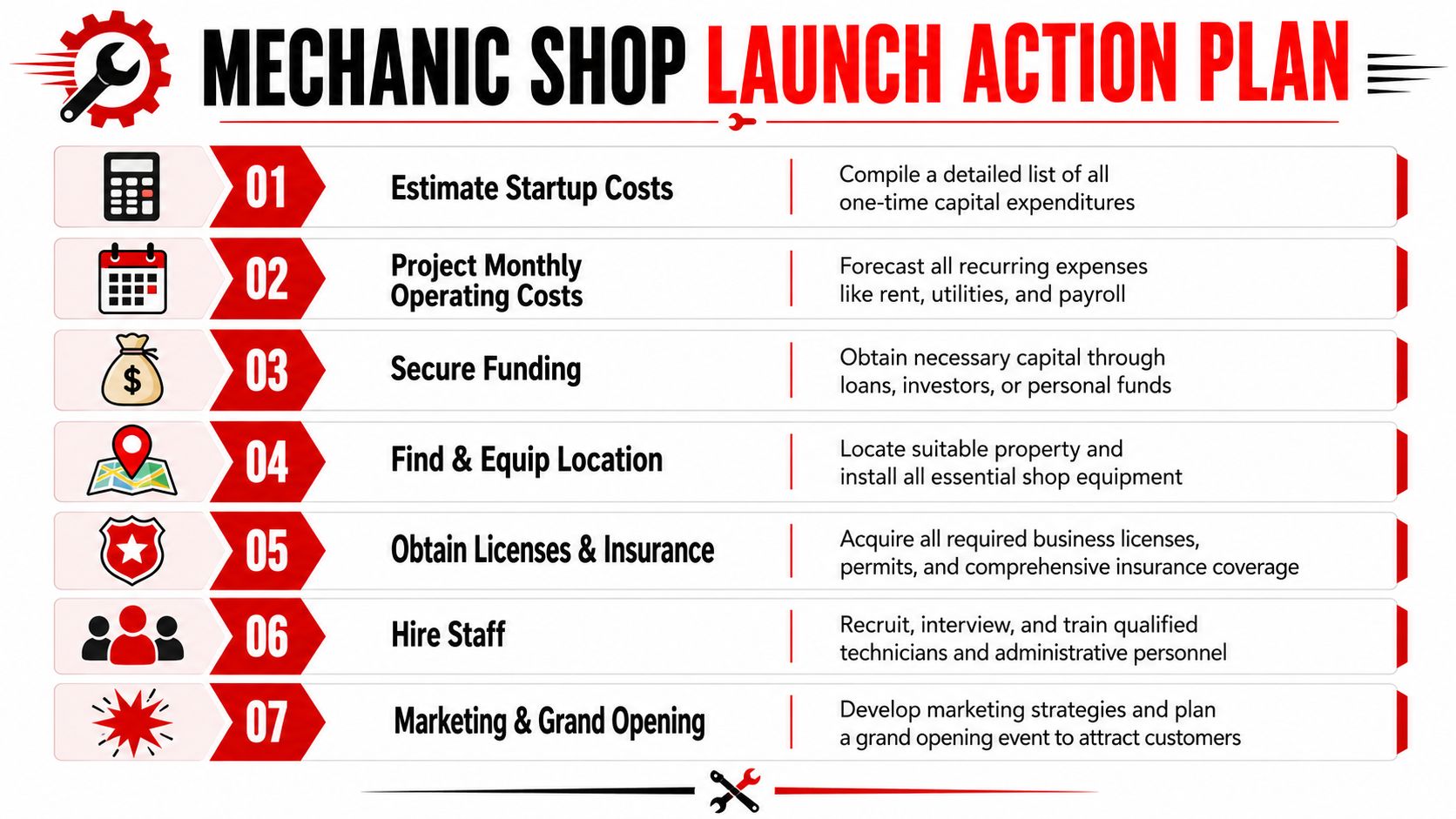

Your Action Plan for Budgeting and Launch

Planning a new shop gets easier when the owner turns the budget into a sequence of decisions. That keeps the launch grounded in operating reality instead of excitement.

A practical launch checklist looks like this:

- Price the opening setup fully. Include tools, lifts, diagnostics, deposits, build-out, insurance, permits, and customer-facing setup.

- Project monthly overhead accurately. Rent, labor, utilities, parts handling, and admin costs need a realistic forecast.

- Separate reserve cash from setup cash. Treat the working capital bridge as protected money.

- Choose the smallest viable operating model. A clean, disciplined shop beats an oversized one with weak cash control.

- Build lender-ready documentation. A line-item budget and reserve plan make financing conversations stronger.

- Set up operations before the first appointment. Intake, inspections, estimates, invoicing, scheduling, and payment collection need structure.

- Launch with measured marketing and tight follow-up. The first months reward shops that answer quickly, document work clearly, and keep approvals moving.

A repair shop rarely fails because the owner didn't know how to fix cars. It fails because the business side never got the same level of attention as the technical side.

If the budget is clear and the reserve is protected, the launch becomes much less risky. That doesn't make ownership easy. It does make the business far more durable.

RedAppy helps repair shops run tighter from first contact to final payment with digital inspections, estimates, invoicing, online payments, inventory visibility, analytics, and a digital shop board built for real workflow. Owners who want a clearer handle on efficiency, revenue tracking, and day-to-day operations can contact RedAppy or review RedAppy's features to see how the platform fits a new or growing shop.

Ready to Transform Your Shop?

RedAppy helps auto repair shops create professional digital estimates with photos and videos, send them instantly via text or email, and get customer approvals in seconds. No credit card required to start.